|

|

1850 M Street NW Suite 300 Washington, DC 20036 202-223-8196 | www.actuary.org Craig Hanna, Director of Public Policy © 2017 American Academy of Actuaries. All rights reserved. |

|

Members of the Social Security Committee include: Timothy Leier, MAAA, FSA, EA—chairperson; Mark Shemtob, MAAA, FSA, EA, FCA—vice chairperson; Robert Alps, MAAA, ASA; Janet Barr, MAAA, ASA; Douglas Eckley, MAAA; Ronald Gebhardtsbauer, MAAA, FSA, EA; Jay Jaffe, MAAA, FSA; Leslie Lohmann, MAAA, FSA, FCIA, EA, ECA; Timothy Marnell, MAAA, ASA, EA; John Nylander, MAAA, FSA; Brendan O’Farrell, MAAA, EA, FSPA, FCA; Jeffery M. Rykhus, MAAA, FSA; Joan Weiss, MAAA, FSA, EA; and Ali Zaker-Shahrak, MAAA, FSA. |

The Social Security Trustees Report is a detailed annual assessment that serves as a basis for discussions of Social Security’s financial problems and their solutions. Social Security’s chief actuary prepares and certifies the financial projections for the Old-Age, Survivors, and Disability Insurance program, under the direction of the Social Security Board of Trustees.

Because future events are inherently uncertain, the report contains three 75-year financial projections to illustrate a broad range of possible outcomes. These projections, each based on a different set of assumptions, are referred to as intermediate, low-cost, and high-cost. The report also provides a sensitivity analysis for key assumptions and a projection based on a probability model (i.e., a stochastic forecast). The trustees consider the intermediate projection to be their best estimate. All information in this issue brief is based on the intermediate projection, unless otherwise noted.

When trust fund reserves are depleted, tax income will be sufficient to provide about three- quarters of the scheduled benefits. The Trustees Report quantifies the value of the benefit and/or tax changes required to restore actuarial balance. Any changes would require congressional action. Failure to act would likely cause a delay in some benefit payouts, which, if not corrected by subsequent congressional action, could result in benefit reductions. However, it should be noted that there is no precedent and no legislative guidance for what would happen if reserve depletion is reached.

|

New Trustees Report Shows No Improvement in OASI and OASDI Trust Funds Depletion Date Social Security’s Financial Soundness Should Be Addressed Now The 2017 Annual Report of the Board of Trustees of the Federal Old-Age (OASI) and Survivors Insurance and Federal Disability Insurance (DI) Trust Funds highlights that:

The sooner a solution is implemented to ensure the sustainable solvency of Social Security, the less disruptive the required solution will need to be.

|

|||||||||||||||||||||||||||||||||

Overview of Financial Status

Short-Range Estimates, 2017–2026

Short-range solvency and financial adequacy are measured separately for Old-Age and Survivors Insurance and Disability Insurance programs, as well as for the combined Old-Age and Survivors Insurance and Disability Insurance (OASDI) trust funds. The trustees have adopted a test for short-range solvency that is based on projected trust fund ratios. A trust fund ratio is the ratio of the trust fund assets at the beginning of the year to the benefits payable during the year. Under the test, a program is considered solvent during any period if the trust fund ratios are positive for each year in the period. A further requirement is that the trust fund ratios remain at or above 100 percent throughout the 10-year short-range period.1 The DI trust fund ratio is 31 percent at the beginning of 2017, and is expected to rise somewhat over the next few years and then decline to 16 percent during 2026. The OASI trust fund ratio is expected to drop from 347 percent at the beginning of the projection period to 187 percent in the 10th year of the projection period.

Social Security’s OASI finances (excluding disability) are somewhat worse than the projection made a year ago. The total change in the projected 10th-year trust fund ratio was a decline of 7 percentage points. Moving the short-range estimate period one year forward accounted for much of the change, because the year dropped from the 10-year projection (2016) had a smaller deficit than the year added to the projection (2026). Other changes, with the impact on the 10th-year trust fund ratio in parentheses, include:

- Moving the short-range estimate period forward one year (reduced ratio by 19 percentage points)

- Changes in economic data and assumptions (reduced ratio by 2 percentage points)

- Changes in demographic data and assumptions (increased ratio by 1 percentage point)

- Changes in programmatic data and assumptions (increased ratio by 9 percentage points)

- Changes in projection methods and data (increased ratio by 6 percentage points)

- Reversal of 2014 executive action on immigration resulting in lower payroll taxes (reduced ratio by 2 percentage points)

Unless otherwise noted, all subsequent information in this issue brief is based on the combined OASDI trust funds.

Trust Fund Asset Reserves

Any excess of tax income over outgo is recorded as an asset reserve of the Social Security trust funds. These trust fund asset reserves are held in special U.S. Treasury securities that totaled $2.8 trillion at the end of 2016. Trust fund asset reserves are expected to increase to almost $3.0 trillion by the end of 2021 (total income including earnings on trust fund assets is projected to exceed benefit payments during that period) and then are projected to decline throughout the remainder of the short-range estimate period and beyond. The bonds in the trust funds represent the government’s commitment to repay the borrowed funds whenever Social Security needs the money.

|

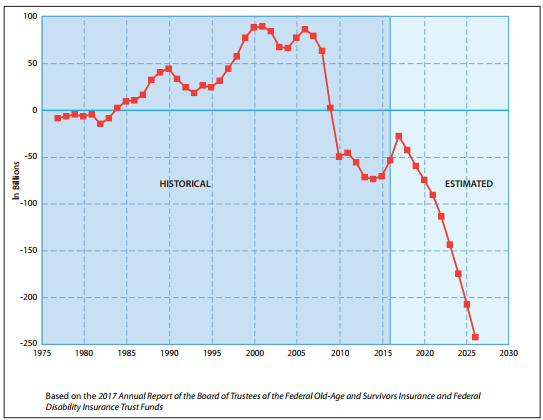

FIGURE 1: OASDI CASH FLOW EXCLUDING INTEREST ON ASSETS

|

Income and Cost

Figure 1 above shows the excess of income (excluding interest) over cost (referred to as a positive cash flow) in the period from 1976 through 2009, and the anticipated excess of cost over income through 2026. Program costs exceeded income (excluding interest) beginning in 2010. The excess of income over cost prior to 2009 has led to the current $2.8 trillion in trust fund asset reserves.

The net annual amounts of income (excluding interest) to, and outgo from, Social Security are expressed in the Trustees Report as percentages of taxable payroll. These percentages are known respectively as the income rate and cost rate. During the short-range estimate period of 2017–2026, the income rate will increase (due to taxation of Social Security benefits) from 13.03 percent to 13.14 percent of annual taxable payroll. The cost rate, meanwhile, will rise from 13.41 percent to 15.37 percent of taxable payroll. The difference between these two rates, called the annual balance, ranges from a deficit of 0.38 percent to a deficit of 2.24 percent2 of taxable payroll during the period from 2017 to 2026.

Long-Range Estimates, 2017–2091

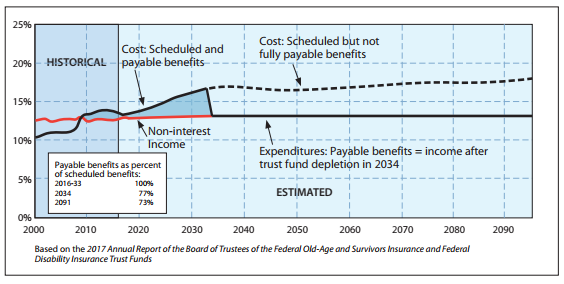

Long-range estimates are based on a 75-year projection that covers the future lifetimes of nearly all current participants, which includes those paying payroll taxes and those already retired. The estimates show that, beginning in 2034, trust fund asset reserves are projected to be depleted and the system is expected to revert to a pay-as-you-go (PAYGO) system. This date is the same as shown in last year’s report. After reserves are depleted in 2034, Social Security income will be sufficient to pay 77 percent of scheduled benefits. This ratio decreases to 73 percent in 2091, as shown in Figure 2.

The projections show expenditures exceeding non-interest income in every year (as has been the case since 2010) and rising rapidly through 2035 as the Baby Boomers retire. While costs are expected to increase quickly, tax revenue is also expected to grow, but more slowly. After 2035, projected costs are fairly level as a share of both GDP and taxable payroll.

|

FIGURE 2: PROJECTED ANNUAL COST AND TAX INCOME AS A PERCENTAGE OF TAXABLE PAYROLL

|

Actuarial balance conveys the long-range solvency of Social Security in one number. It can be described as the amount of additional or excessive income as a percent of taxable payroll that would bring the program’s finances in balance. Actuarial balance is the present value of all income less all costs, divided by the present value of the taxable payroll over the year period. It represents the annual amount (expressed as a percent of taxable payroll) by which income would need to increase to have trust fund assets equal to one year of scheduled benefits at the end of the 75-year projection period. The actuarial balance worsened, from a negative 2.66 percent to a negative 2.83 percent, from the 2016 to the 2017 Trustees Report. Refer to the appendix for a more expanded definition of actuarial balance.

The long-range expected increase in Social Security program costs relative to program income is principally caused by demographic trends. These demographic trends are very well- known and are generally referred to as “aging” or, sometimes, as “the aging of America.” It is useful to further separate the aging trend into two components:

| (i) | macro-aging, which is observed at the population level and refers to a shift in the age distribution of the population caused by the large one-time decrease in birth rates beginning in the mid-1960s (the fertility drop after the large Baby Boom generation); and |

| (ii) | micro-aging, which can be observed at an individual level and refers to the expected long-term increase in life expectancies caused by individuals living longer, on average, in each succeeding generation. |

A third demographic component, which acts to partially offset macro-aging, is net immigration. Because immigrants tend to be younger, higher immigration can offset some of the change in the age distribution of the population caused by lower birth rates.

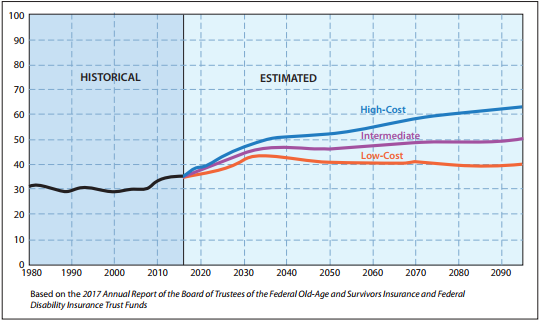

The ratio of covered workers to Social Security beneficiaries is expected to decrease significantly from 2.8 in 2016 to 2.2 in 2035, primarily due to macro-aging, and then micro-aging will cause the ratio to decrease, albeit more slowly, to 2.0, by the end of the 75-year projection period. This decrease over the projection period of approximately 30 percent is important in a system in which the dollars paid in must equal the dollars paid out—a PAYGO system.

Figure 3 shows the projected growth in the number of Social Security beneficiaries relative to the covered working population, under the three sets of assumptions. Because the program financing is nearly PAYGO, the three alternative projections of long-range cost show similar patterns.

|

FIGURE 3: NUMBER OF SOCIAL SECURITY BENEFICIARIES PER 100 WORKERS

Low-cost, intermediate, and high-cost projections. |

The Social Security Committee of the American Academy of Actuaries believes that any modifications to the Social Security system should include sustainable solvency as a primary goal. Sustainable solvency means that not only will the program be solvent for the next 75 years under the reform methods adopted, but also that the trust fund reserves at the end of the 75-year period will be stable or increasing as a percentage of annual program cost. Refer to the appendix for a more complete explanation of sustainable solvency.

Providing for solvency beyond the next 75 years will require changes to address micro-aging, as beneficiaries will likely be receiving benefits for ever-longer periods of retirement.

Regardless of the types of changes ultimately enacted into law, measures to address Social Security’s financial condition will best serve the public if implemented sooner rather than later. Some advantages of acting promptly are:

- Future beneficiaries gain time to plan for all aspects of retirement and modify their own financial planning, while adjusting to legislated changes in Social Security.

- Implementation of program changes can be more gradual and span multiple generations of retirees.

- Public trust in the financial soundness of the Social Security program will improve.

Appendix

Other Measures of Financial Status

The metrics used by the trustees to present the program’s financial status are discussed in more detail below.

Actuarial Balance

Actuarial balance is calculated as the difference between the summarized income rate and the summarized cost rate over a period of years.

The summarized income rate is the ratio of any existing trust fund plus the sum of the present value of scheduled tax income for each year of the period to the sum of the present value of taxable payroll for each year of the period. The summarized cost rate is the ratio of the sum of the present value of cost for each year of the period, including one year’s outgo at the end of the period, to the sum of the present value of taxable payroll for each year of the period. Table 1 shows the components of actuarial balance.

In the 75-year period, 2017–2091, the actuarial deficit is 2.83 percentage points. The actuarial deficit increased from the comparable figure of 2.66 percentage points a year ago due to a combination of factors, including changes in demographic data and assumptions, changes in economic data and assumptions, and legislative and policy changes.

TABLE 1: LONG-RANGE ACTUARIAL BALANCE

(percentage of taxable payroll)

|

Period

|

Summarized Income Rate

|

Summarized Cost Rate

|

Actuarial Balance (percentage points)3

|

|

25-year (2017-41)

|

14.65%

|

16.32%

|

-1.67

|

|

50-year (2017-66)

|

14.02%

|

16.44%

|

-2.42

|

|

75-year (2017-91)

|

13.84%

|

16.67%

|

-2.83

|

|

Based on the 2017 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds

|

|||

An immediate increase of 2.76 percentage points in the payroll tax (from 12.4 percent of payroll to 15.16 percent of payroll), a benefit reduction of about 17 percent, or some combination of the two, would pay all benefits during the period, but would not end the period with any trust fund reserve.

The high-cost 75-year projection in the Trustees Report shows a far greater actuarial deficit—6.63 percent of taxable payroll. The low-cost projection is much more favorable, with a small positive actuarial balance for the 75-year period.

Trust Fund Ratios

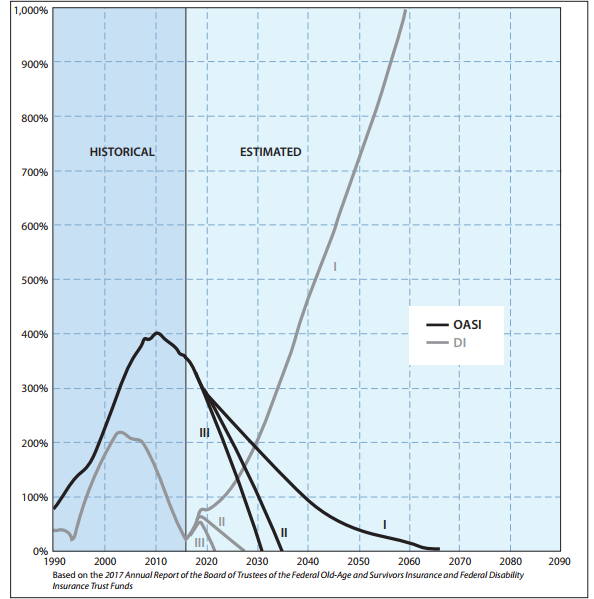

The trust fund ratio, equal to trust fund assets as a percentage of the following year’s cost, is an important measure of short-term solvency. A trust fund ratio of at least 100 percent indicates the ability to cover the expected scheduled benefits and expenses for the next year without any additional income. Figure 4 shows projected trust fund ratios under all three sets of assumptions.

|

FIGURE 4: LONG-RANGE PROJECTIONS OF TRUST FUND RATIOS—OASI AND DI SHOWN SEPARATELY

Low-cost, intermediate, and high-cost projections are labeled I, II, and III, respectively (assets as a percentage of annual cost). |

As a measure of long-range solvency, the trust fund ratio shows when the program is expected to deplete reserves and become unable to pay full benefits scheduled under current law. Though Figure 4 illustrates the OASI and DI trust fund ratios separately, the combined OASDI trust fund reserve depletion (not shown in Figure 4) occurs in 2034 under the intermediate projection.

Sustainable Solvency

Sustainable solvency means the program is not expected to deplete reserves any time in the 75-year projection period, and trust fund ratios are expected to finish the 75-year projection period on a stable or upward trend.

Sustainable solvency is a stronger standard than actuarial balance in two ways. First, actuarial balance is based on averages over time, without regard to year-by-year figures that could indicate inability to pay full benefits from trust fund assets at some point along the way. Second, actuarial balance can exist even when trust fund ratios toward the end of the period are trending sharply downward.

Sustainable solvency, in contrast, requires strict year-by-year projected solvency AND trust fund ratios that are level or trending upward toward the end of the period. For example, following the last major Social Security reform in 1983, the 1983 Trustees Report projected a positive actuarial balance under the intermediate assumptions, but the annual balances were negative and declining at the end of the 75-year period. That report was in actuarial balance but did not show sustainable solvency. As a result, the actuarial balance generally has been declining since then, primarily as a consequence of the passage of time. It is important to note that this result was exactly what the Trustees Report projected in 1983. More than 30 years later, it should be no surprise that large and growing actuarial deficits are now projected at the end of the long-range projection period. Adequate financing beyond 2091, or sustainable solvency, would require larger program changes than needed to achieve actuarial balance.

Unfunded Obligation

The unfunded obligation is another way of measuring Social Security’s long-term financial commitment. To compute it, discount with interest the year-by-year streams of future cost and income and then sum them to obtain their present values. Based on these present values, the general formula for computing the unfunded obligation is:

| Present value of future cost (benefits and expenses) minus the present value of future income from taxes minus current trust fund assets. |

The unfunded obligation may be computed and presented in several ways. Perhaps the most useful way is based on taxes and benefits for an open group of participants over the next 75 years, including many people not yet born, the same as was calculated in the basic projections. That methodology is consistent with the primarily pay-as-you-go way the program is designed and currently run. Although the trustees provide alternative calculations based on the closed group of current participants, we believe the open- group basis avoids certain misleading outcomes. For example, if the program were in exact actuarial balance, the open-group measure of the unfunded obligation would be zero, while the closed-group measure would show a substantial unfunded obligation.

The dollar amount of unfunded obligation is easier to interpret if put in perspective—for example, by comparing it with the size of the economy over the same period. The unfunded obligation is often presented as a percentage of the present value of either taxable payroll or of gross domestic product (GDP). At the beginning of 2017, the open-group unfunded obligation over the next 75 years was $12.5 trillion (up from $11.4 trillion last year). This now represents 2.66 (2.49 last year) percent of taxable payroll, or 0.9 percent (same as last year) of GDP.

In recent years, the Trustees Reports have also presented the unfunded obligation based on stretching the 75-year projection period into infinity. The infinite horizon projections project all annual balances beyond 75-years assuming that the current law, demographic assumptions, and economic trends from the 75-year projection continue indefinitely; in practice, this is highly problematic. Projections over an infinite time period have an extremely high degree of uncertainty. Troublesome inconsistencies can arise among demographic and program-specific assumptions. By assuming that longevity keeps increasing forever while retirement ages remain static, for example, the infinite time period forecast will eventually result in an extremely long period of retirement.

Measures of Uncertainty

Because the future is unknown, the trustees use alternative projections and other methods to assess how the financial results may vary with changing economic and demographic experience.

Alternative Sets of Assumptions

Table 2 shows a comparison between recent values and ultimate long-range values of five key assumptions used in each of the three projections. With the exception of productivity growth, where the ultimate values have not changed from last year’s report, the ultimate values of the other assumptions exhibit some minor changes when compared to last year’s Trustees Report.

|

TABLE 2: CURRENT AND LONG-RANGE VALUES OF KEY ECONOMIC AND DEMOGRAPHIC ASSUMPTIONS

Based on the 2017 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds * 10-year average, except productivity growth and real-wage growth, which are measured from 2008.

|

|||||||||||||||||||||||||||||||||||||||

Sensitivity Analysis

The low-cost and high-cost projections change all the major intermediate assumptions at once in the same direction, either favorably or unfavorably. In contrast, there might be some interest in how the projections change when only one key assumption is changed at a time, either favorably or unfavorably. A sensitivity analysis shows exactly this. Just one assumption is changed at a time to determine the financial impact. Table 3 gives results of three sensitivity tests focusing on total fertility rate, mortality reduction, and real-wage growth.

A significant component of the differences between low-cost, intermediate, and high-cost projections is the real-wage growth (specifically the difference between inflation and real wages, or the real-wage differential). Actuarial balances at all durations as well as the projected depletion dates change materially based on changes to this component.

If the real-wage growth assumption were changed from 1.20 percent to 1.82 percent, for example, the actuarial deficit would be reduced from 2.83 percent of taxable payroll to 1.78 percent, and the year of trust fund asset reserve depletion would be extended from 2034 to 2037.

|

TABLE 3: SENSITIVITY TO VARYING ANY OF THREE KEY ASSUMPTIONS

Based on the 2017 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

Statement of Actuarial Opinion

The Trustees Report concludes with the Statement of Actuarial Opinion, which is the Social Security chief actuary’s certification that calculations and assumptions used and the resulting actuarial estimates are, individually and in the aggregate, reasonable for the purpose of evaluating the actuarial status of the trust funds, taking into consideration the past experience and future expectations for the population, the economy, and the program.

The Statement of Actuarial Opinion included with the 2017 Trustees Report addresses the inconsistency between trust fund accounting and unified budget accounting.

References

American Academy of Actuaries issue briefs on Social Security

Annuitization of Social Security Individual Accounts (November 2001)

| 1. |

This condition applies when the trust fund ratio is at least 100 percent at the beginning of the period. If the trust fund ratio is below 100 percent at the beginning of the period, the test of short-term financial adequacy requires that the trust fund ratio increase to 100 percent within five years (while remaining positive at all times) and then remain at or above 100 percent for the rest of the short-range period. |

| 2. |

Table IV. B1, 2017 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds. Please note that due to rounding, numbers may not add up. |

| 3. |

The results shown in the Actuarial Balance column may not be equal to the difference between Summarized Income Rate and Summarized Cost Rate because of rounding. |