|

|

|

The PBGC program that guarantees minimum benefits to multiemployer pension plan participants is projected to exhaust its assets within approximately eight years.

If the PBGC multiemployer program exhausts its assets, beneficiaries and retirees receiving PBGC support could see their guaranteed benefits reduced by approximately 85 percent.

The multiemployer program’s financial stresses stem from inadequate premium levels, maturing pension plans, industry transformations, and the 2008 recession.

Based on PBGC’s 2016 MPRA report, premiums would need to increase approximately 6 times current levels to cover expected financial assistance payments through 2035, with even larger increases necessary to ensure long-term sustainability.

There are no easy solutions, but doing nothing means that ultimately the PBGC guarantee will not be honored.

1850 M Street NW

Suite 300

Washington, DC 20036

202-223-8196 | www.actuary.org

Craig Hanna, Director of Public Policy

Ted Goldman, Senior Pension Fellow

© 2016 American Academy of Actuaries All rights reserved.

|

Members of the Pension Practice Council include: Noel Abkemeier, MAAA, FSA; Michael Bain, MAAA, FCA, ASA, EA, FSPA; Bruce Cadenhead, MAAA, FSA, FCA, EA; Donald Fuerst, MAAA, FSA, FCA, EA; Tim Geddes (Vice Chairperson), MAAA, FSA, FCA, EA; William Hallmark (Chairperson), MAAA, FCA, ASA, EA; Kenneth Hohman, MAAA, FSA, FCA, EA; Eric Keener, MAAA, FSA, FCA, EA; Ellen Kleinstuber, MAAA, FSA, FCA, EA, FSPA; Timothy Leier, MAAA, FSA, EA; Thomas Lowman, MAAA, FSA, FCA, EA; Tonya Manning, MAAA, FSA, FCA, EA; Alan Milligan, MAAA, FSA, FCA, FCIA; Andrew Peterson, MAAA, FSA, FCA, EA; Steven Rabinowitz, MAAA, FSA, FCA, EA; Francis Ratnasabapathy, MAAA, FSA, FIAA; John Schubert, MAAA, FCA, ASA; Josh Shapiro (Vice Chairperson), MAAA, FSA, FCA, EA; James Verlautz, MAAA, FSA, FCA, EA. Christian Benjaminson, MAAA, FSA, FCA, EA, and Jason Russell, MAAA, FSA, EA, assisted with the drafting of this issue brief. |

Honoring the PBGC Guarantee for Multiemployer Plans Requires Difficult Choices

Executive Summary

The Pension Benefit Guaranty Corporation (PBGC) is a federal agency that guarantees minimum benefit payments to participants in multiemployer pension plans 1 if those plans become insolvent. Multiemployer pension plans are those covering employees in unionized industries from more than one employer, typically companies from the same industry.

The maximum guaranteed level of benefit is approximately $13,000 per year for a participant with 30 years of service, and is lower for participants with fewer years of service or monthly accrual rates averaging below $44 per year of service. Despite the modest guarantee level, PBGC’s multiemployer program itself is projected to become insolvent (unable to pay its full guarantee) within approximately eight years. If the guarantee is to be honored in full, action needs to be taken to increase the resources available to PBGC in order to support the multiemployer guarantee and/or reduce the need for PBGC financial assistance to insolvent plans.

Resources to provide the guaranteed benefits have come from premiums charged to multiemployer plans on a flat per-participant basis. It is evident that historical premium rates were insufficient to adequately cover the cost of providing the guarantee to insolvent multiemployer plans. According to the PBGC figures in the 2016 MPRA Report, aggregate premiums would need to increase by roughly 6 times the current level in order to support the guarantee for the next 20 years, with larger increases necessary for longer-term solvency. Larger increases would also be needed to protect against experience that is worse than expected. Such increases would charge current active participants and employers for the guarantee promised to, but not reserved for, prior generations of participants and employers. Assessing premiums that would require an increase in current contributions made by employers as part of the active participants’ wage and benefit package to pay for historical guarantees risks the further withdrawal of participation in the multiemployer system. For this reason, there is a danger that raising per-participant premiums too high will result in additional instability and a reduction, rather than an increase, in benefit security.

|

|

|

This issue brief explores how the multiemployer guarantee system evolved to its current position and identifies options to consider going forward. Reform options include premium increases in a variety of structures, resources from outside the system, and alternatives that could increase the stability of ongoing multiemployer plans in an effort to reduce the need for PBGC financial assistance. None of the options are ideal, and they require difficult sacrifices, possibly from parties who had no role in the creation of the problem. But it is clear that if nothing is done, the guarantees promised to the participants in multiemployer plans will not be fully honored.

Key Developments and Drivers Leading to the Current Situation

The financial challenges facing PBGC’s multiemployer system are the result of many factors and complexities. These include:

Inadequate premium levels: The per-participant premium levels have not adequately reflected the cost of providing the guarantees. While this is obvious with the advantage of hindsight, the cost of providing the guarantees is very difficult to predict. The PBGC reported a surplus in the multiemployer program for roughly the first 20 years of its existence, and the reported deficit, which was reported as less than $1 billion until 2010, is now currently over $50 billion.

Inadequate withdrawal liability payments: Employer bankruptcies can damage multiemployer plans because withdrawal liability is often paid at pennies on the dollar in bankruptcy. There are also several statutory restrictions in ERISA on the assessment and collection of withdrawal liability that can prevent a plan from collecting the full amount of a withdrawing employer’s share of the plan’s unfunded vested liability. These factors shift the benefit cost to the remaining contributing employers. This shift would be a less significant issue if withdrawing or bankrupt employers were replaced in the plan by new employers of similar size. However, if new employers do not replace withdrawn or bankrupt employers, one or more significant withdrawals or bankruptcies among the sponsors of a multiemployer plan can eventually lead to the insolvency of the plan and the need for PBGC financial assistance.

Alignment of risks and inadequate contributions: Ongoing multiemployer plans typically invest in a diversified portfolio of assets, resulting in lower revenue needed from contributions than if they had invested in a default-free matching portfolio. Plans determine funding needs by discounting future payments using an assumed rate of investment return. Current rates are typically between 7.0 and 7.5 percent. This approach creates a risk, if investment returns are less than the assumed return, that additional contributions will be required in order to provide the benefits. In addition, to the extent there are net experience losses (from either economic or demographic assumptions), these losses were historically amortized over relatively long time periods. These risks may be supportable in plans that maintain strong bases of contributing employers, but can be unmanageable in less stable plans. For many plans, these factors have led to underfunding and the additional contributions needed to become fully funded are not affordable.

Maturing plans: As plans mature, they have far more inactive participants than active participants and the total liability of the plan becomes very large compared to its contribution base. As a result, any variations in experience or changes in assumptions become more difficult to manage with additional contributions. A certain degree of maturity is the natural path of a pension plan, but the maturity level can be exacerbated by the withdrawal of employers from participating in the plan either due to the decline of an industry or the unwillingness of employers to continue to be exposed to the risks associated with participating in these plans. As the contribution base declines compared to the total liability, the inherent risks of the investment policy and other actuarial assumptions are magnified.

Industry transformation: Many multiemployer plans are part of industries that have experienced changing business environments (e.g., deregulation, technology transformations, globalization, less unionization) that have vastly altered the workforce covered by those plans. The resulting decline in the number of participating employers and employees has further weakened the financial position of affected multiemployer plans.

The 2008 financial crisis: The “Great Recession” has had a lasting impact on many multiemployer pension plans, some of which were still recovering from 2000-2002 market events, simultaneously exposing a number of different risks in the system. Not only were assets depleted through investment losses, but the financial crisis impact on some covered industries resulted in an even smaller contribution base from which to restore the health of the plans. Furthermore, the lingering low-interest-rate environment resulting from the recession has made it more unlikely that investment returns over the next few years will pay as large a share of plan costs as was anticipated. Many plans that could have recovered from either the asset losses or the low interest rates or the declines in their industries find themselves unable to effectively deal with the events concurrently. For some of the more mature plans, recovery is not possible without financial assistance.

These issues have been developing over time. Combined, they have stressed most multiemployer plans and placed PBGC’s multiemployer program in a precarious position.

Steps Taken to Strengthen the Multiemployer Program: MPRA

In response to the projected insolvency of some multiemployer plans and the impact on PBGC’s multiemployer program, the Multiemployer Pension Reform Act (MPRA) was enacted in December 2014. Highlights of the MPRA law include:

Suspension of benefits: MPRA created a new category of at-high-risk multiemployer plans. In general, a plan is in critical and declining status if it is projected to deplete all of its assets within 20 years. The sponsor of a plan in critical and declining status is allowed, but not required, to apply to the Department of Treasury to suspend a portion of its benefits—in other words, permanently or temporarily reduce accrued benefits, potentially including some benefits being paid to current retirees and beneficiaries. To be eligible for a suspension, the plan sponsor must exhaust all other reasonable measures to avoid insolvency, and the suspension must be sufficient for the plan to be projected to remain solvent over an extended period of at least 30 years.

MPRA imposes a number of restrictions on the suspensions. For example, benefits may not be reduced below 110 percent of a participant’s PBGC guarantee level, and suspensions must be equitably distributed across participants and may not exceed the level required to reasonably enable future solvency. Furthermore, protections apply to participants and beneficiaries age 75 and older, as well as plan disability benefits.

Any proposed suspension of benefits is subject to review and approval by the Department of Treasury. If Treasury approves the proposed suspension, the suspension is then subject to a vote by plan participants. If the participant vote rejects the suspension and the plan is deemed to be “systemically important” (representing at least $1 billion in projected liabilities to PBGC), Treasury must override the vote and implement the proposed suspension.

Partitions and facilitated mergers: Under MPRA, the sponsor of a plan in critical and declining status may also apply to PBGC for financial assistance through a partition. Under a partition, PBGC immediately takes on responsibility for paying a portion of the benefits. In order to receive a partition, the plan sponsor must take all reasonable measures to avoid insolvency, including suspending benefits to the maximum extent allowed under MPRA. In order to grant a partition, PBGC must certify that the partition will reduce its own long-term loss, does not impair its ability to provide financial assistance to other plans, and is necessary for the plan to remain solvent over an extended period of at least 30 years. Facilitated mergers of two or more plans represent an additional mechanism for PBGC to provide financial assistance to troubled plans, and the use of this provision is subject to requirements similar to partitions.

Increased premiums: In addition to providing new tools to plans in critical status, MPRA doubled the flat-rate premium that all multiemployer pension plans must pay annually to PBGC. Specifically, the per-participant premium rate increased from $13 to $26 for plan years beginning in 2015. The premium rate will increase automatically each year with inflation (it is $27 in 2016). In the FY 2015 Projections Report, PBGC estimated the present value of projected premiums over the next 10 years to be about $2.7 billion as of Sept. 30, 2015.

While these activities improve PBGC’s financial position, the 2016 PBGC MPRA Report confirms they fall well short of placing the program on firm ground, especially in light of decisions since the passage of MPRA.

Recent and Pending Developments

Several key developments have occurred since the passage of MPRA that have dampened the potential relief that MPRA was expected to provide. In addition there are two additional issues that are yet to be determined.

Central States application denial: The Central States Pension Fund is widely understood to be the single largest potential liability to PBGC’s multiemployer program. The plan covers in excess of 400,000 participants and is expected to become insolvent within the next decade. Central States submitted an application to Treasury to suspend benefits under MPRA in late September 2015. On May 6, 2016, the Treasury Department denied the Central States application, citing, among other reasons, that the proposed benefit suspensions were “not reasonably estimated to allow the plan to avoid insolvency.” Subsequent to Treasury’s decision, Central States posted

a letter to its employees indicating that it will not reapply, thus likely placing a significant burden on PBGC—a burden that MPRA had been anticipated to reduce.

Local 707 application for partition and benefit suspensions denied: PBGC informed the Board of Trustees for the Road Carriers—Local 707 Pension Fund that its application for partition under MPRA had been denied. The Local 707 plan is expected to run out of money to pay benefits in February 2017. In June 2016, PBGC concluded that the contribution base units, active participant counts, and contribution levels projected in the application were based on “unreasonably optimistic assumptions.” While the impact on PBGC from this decision alone is minimal, with each denial, the relief anticipated for PBGC through MPRA appears to be less certain. Following PBGC’s denial for the request for partition, Treasury has also denied Local 707’s application for benefit suspensions. Given the expected short period to insolvency, the Local 707 situation may not be a good indicator of the potential relief MPRA may have to offer other plans.

Key issues yet to be determined include:

Possible relief for Mine Workers: The plan widely considered to be the second-largest potential liability to PBGC’s multiemployer program is the United Mine Workers of America (“UMWA”) 1974 Pension Plan. Due to the relatively low benefit levels under the 1974 plan—MPRA requires a maximum suspension of 110 percent of PBGC guarantee levels—the UMWA plan is not a candidate for benefit suspensions under MPRA. Furthermore, it is expected that any partition of the 1974 plan would be too large for PBGC’s multiemployer program to sustain.

Proposals have been made to provide relief to the 1974 plan (as well as health plans covering retired members of the UMWA and their families) in the form of additional financing. For example, the president’s fiscal year 2017 budget proposal includes a provision to make annual transfers from the Abandoned Mine Reclamation Fund to the UMWA Health and Retirement Funds. If this proposal were to be enacted, the annual transfers may be sufficient to ensure the long-term solvency for the 1974 plan. The 1974 plan would therefore no longer be a PBGC liability. The likelihood of such a proposal becoming law is unclear, but if passed, it would have a significantly positive impact on PBGC’s multiemployer program.

Future commitment to the pension system: Multiemployer plans have had very few new employers adopt new plans or join existing plans in recent years, and many plans are also struggling to retain their current employer base. Employer withdrawals tend to reduce the financial strength of plans, while also gradually reducing the number of participants on which PBGC premiums are based. It is important that the employers and co-sponsoring unions participating in the multiemployer plan system remain in the system and continue to provide retirement benefits to employees in a way that does not further jeopardize PBGC’s financial assistance program. Achieving this objective may require new developments and innovations that will allow employers to remain in the multiemployer system while protecting their businesses from financial risks and competitive disadvantages. Such developments might include the adoption of risk-sharing pension plan designs and possible revisions to contribution requirements and withdrawal liability provisions that limit the transfer of liability to the remaining employers. Any new approach adopted must be scrutinized carefully to assure it will strengthen, rather than weaken, the overall PBGC multiemployer financial assistance program.

Moving Forward—Factors for Consideration

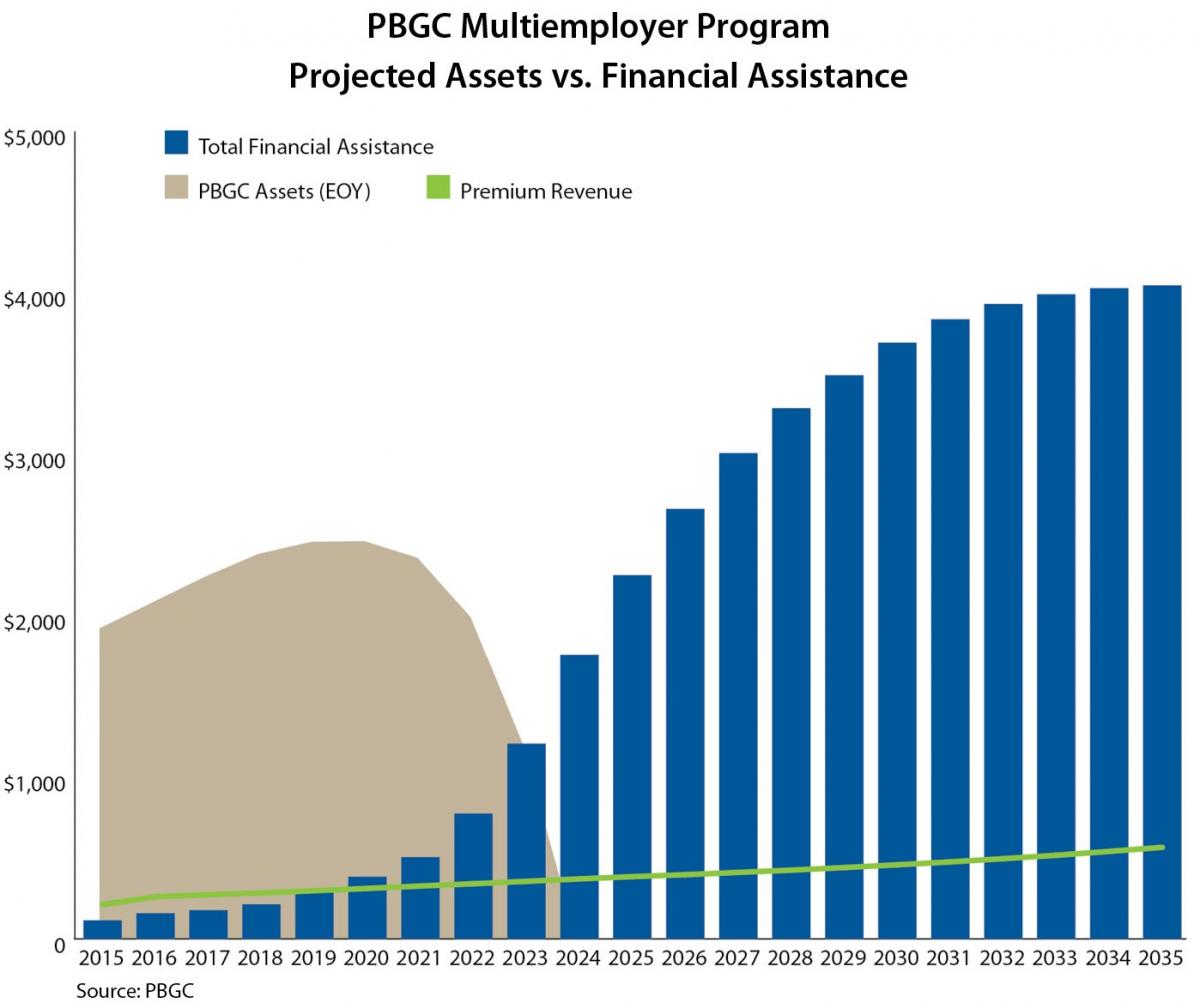

If PBGC’s multiemployer program exhausts its assets, which absent legislative action appears to be inevitable, the agency will only be able to provide financial assistance to insolvent plans to pay benefits and administrative expenses that are equal to the annual revenues it receives. At a current premium rate of $27 per participant, the annual premium revenue is approximately $260 million. While multiemployer financial assistance payments were $103 million in fiscal year 2015, this figure is expected to increase rapidly in the coming years as more plans reach the point of insolvency. According to PBGC’s 2016 MPRA Report, annual financial assistance is projected to exceed $200 million by 2018, exceed $2 billion by 2025, and reach roughly $4 billion by 2034.

|

The graph above shows PBGC’s average projection results.2 The projected financial assistance is shown by the stacked bars, premiums by the light green line, and projected assets by the tan area. Current insolvent plans (dark orange bars) and terminated plans that are expected to become insolvent (light blue bars) make up a very small portion of the projected financial assistance. The largest troubled plan (dark gray bars) does not currently require any financial assistance, but when it does, the level of financial assistance required would, by itself, move PBGC into insolvency. The gray bars grade up as PBGC assesses an increased likelihood of this plan becoming insolvent, peaking in 2030. The second-largest troubled plan (light orange bars) is not expected to seek relief under MPRA. This projection assumes that no benefit suspensions or partitions are approved. In its annual report, PBGC books a liability for plans that it expects to become insolvent within 10 years. The financial assistance for these plans is represented by the green bars. The dark blue bars represent financial assistance for other plans based on PBGC’s projection model. In order to restore the sustainability of PBGC’s guarantee, either revenues need to increase significantly or the projected financial assistance needs to be reduced significantly (preferably by reducing the need for financial assistance); most likely, both need to occur.

While there is little uncertainty that, without intervention, PBGC’s multiemployer program will exhaust its assets, there is considerable uncertainty regarding both the timing of this failure and the amount of money that would be needed to prevent it. Aside from the possibility of congressional action, some of the most significant factors that affect these uncertainties are:

-

The extent to which plans are able to avoid insolvency by using the MPRA suspension, partition, and facilitated merger provisions.

-

The ability of plans to increase contribution revenue by maintaining or expanding their bases of employers, raising contribution rates, and collecting withdrawal liability.

-

The investment returns that plans earn on their assets.

Ability to use MPRA for benefit reductions and suspensions: While MPRA introduced several tools for troubled plans to use to avoid insolvency, there is considerable uncertainty regarding the number of these plans that will take advantage of these tools. First, the use of these tools is not mandatory, so plan trustees, and in some cases plan participants, need to make a decision to use them. If the plans decide they want to use one of these tools, it is not clear how many will be able to satisfy the criteria that MPRA and associated regulations established for each tool. We already know that the Central States Pension Fund is not likely to use the MPRA tools.

In addition to benefit suspensions, the other MPRA tools for deeply troubled multiemployer plans are partitions and facilitated mergers. Both of these provisions involve PBGC using some of its assets prior to the point when a plan becomes insolvent, with the goal of preventing that insolvency. A significant requirement for PBGC to implement partitions and facilitated mergers is that the outcome must reduce PBGC’s long-term liabilities and must not impair its ability to provide financial assistance to other plans.

In the FY 2015 Projections Report, PBGC projects only a $3 billion reduction in its deficit in 2025 based on its current best estimate of future suspensions and partitions. The 2014 Projections Report had estimated a $16 billion reduction in its deficit in 2024 based on its prior (more optimistic) estimate of future suspensions and partitions. The denial of the Central States application and other events have reduced the projected positive impact on the sustainability of PBGC’s guarantee and as a result, the ultimate impact of MPRA is uncertain.

Increase contribution revenue by plans: The trustees of troubled multiemployer plans are required under the Pension Protection Act of 2006 to establish one or more schedules of contribution rates and accompanying benefit levels from which the bargaining parties may choose. The purpose of these schedules is to establish minimum contribution levels that all employers must satisfy in order to continue in the plan. The trustees often face a very difficult decision in determining the appropriate contribution levels. Assuming there will be no changes in the active participant population size and the employers that contribute to the plan, higher contributions for a given benefit level make it more likely that the plan will recover and participant benefits will be secure. But if the trustees set the contribution rates too high, it could drive employers and active members out of the plan, which may have the opposite effect on funding levels and benefit security.

Contribution revenue for multiemployer plans is also affected by the number of hours, or another measure of employment level, that active participants work in covered employment. For example, if the contribution rate goes up by 10 percent, but active participants work 10 percent fewer hours, then the dollar amount of contribution revenue will remain essentially flat. Withdrawal liability payments made to a plan by former employers are an additional component of the contribution revenue, and an additional source of uncertainty. Given these complexities, projecting revenue into the future is especially difficult.

If the economy improves, it is possible that contributions into underfunded multiemployer plans could increase rapidly, as a strong economy will increase both the employment level of the covered workforces and the possibility of higher contribution rates. Furthermore, a strong economy may result in employers shoring up unfunded legacy obligations but exiting the multiemployer system prospectively. But if the economy remains weak, or deteriorates further, underfunded plans could have difficulty even maintaining their current contribution levels. In addition, the level of future union membership in some industries is an important factor in the ability of plans to recover. These variables could have a significant impact on the level of premium increases necessary to prevent PBGC’s multiemployer program from exhausting its assets.

The vast majority of multiemployer pension plans are not reasonably expected to become insolvent. It is critically important to PBGC’s long-term financial success that these plans continue to pay both the targeted benefits and PBGC premiums into the future.

Investment returns on plan assets: Multiemployer plans have two sources of income: employer contributions (including employer withdrawal liability payments), which are discussed in the previous section, and investment returns. For many multiemployer plans today, the vast majority of their expected income is from their anticipated investment returns. When anticipated investment returns do not materialize, it is very difficult to make up for the shortfall with additional contributions because the shortfall in a given year is often a multiple of annual contributions.

In addition, significant negative cash flow (paying more in benefits and expenses than what is collected by contributions) makes it difficult to make up for a shortfall with future good investment returns because the asset base is diminishing over time. Many multiemployer plans have significant negative cash flows and are thus very sensitive to short-term investment returns.

The reliance of plans on investment returns as their primary source of income coupled with the volatility of these returns make them an important factor in evaluating PBGC’s financial challenges. If plan sponsors are unable to make up for investment losses with higher contributions or future investment returns, PBGC’s guaranteed benefits become increasingly important to plan participants.

Considerations for Legislative Action

While the plan-level events identified above could cause the situation to improve, the president and Congress can also play a role in finding a solution. The most direct approach to improve the finances of PBGC’s multiemployer program would be to consider legislation to increase premiums. As part of MPRA, the annual premium level increased from $13 per participant to $26 per participant, effectively doubling the projected premium revenue and modestly extending PBGC’s projected insolvency date. In theory, the deficit in the program could be eliminated by simply raising the premium rate. However, in practice, the level of increase that would be necessary is likely to be so large that it may cause more problems than it solves. PBGC’s 2016 MPRA Report indicates that premiums would need to be increased by as much as six times the current level in order to avoid insolvency over the 20-year projection period, with larger increases necessary to achieve longer-term solvency or to protect against unexpected adverse experience.

There are at least two potential problems that could be caused by higher premium levels. The first is that for plans that are struggling to postpone insolvency or improve their funding levels, a large increase in the premium rate will accelerate insolvency or make recovery more difficult as assets that could be used to support benefits are diverted to PBGC. A second problem is that the companies and employees who bargain over contributions to the plans may feel that the increased premium level makes the pension plan no longer cost-effective, which could motivate them to move towards defined contribution plans, resulting in lower premium collections and potentially higher financial assistance needs.

The current multiemployer premium is entirely calculated on a flat-dollar per-participant basis, with the levels of benefit provided by a particular plan playing no role in the premium amount. Plans that provide lower benefits pay a premium that is a greater percentage of plan costs than is the case for a plan that provides larger benefits. In addition to the inequity of paying the same premium amount for a proportionally smaller guarantee, it is more difficult for plans at the low end of the benefit spectrum to afford additional premiums than it is for plans with more generous wage and benefit packages.

An increase in the multiemployer premium rate is not restricted to simply increasing the flat per-participant amount. A variety of other approaches have been discussed, most notably in the president’s budget proposal for the 2017 fiscal year, which also includes a recommendation to grant the PBGC board the authority to set premiums.

Potential approaches include:

|

Type of Premium |

Key Advantages |

Key Disadvantages |

|

Variable premium that depends on the funded position of the plan |

Links premiums to PBGC’s exposure. |

Larger premiums for plans least able to afford them and may accelerate insolvency for troubled plans. |

Variable premium that depends on the size of the benefits provided

by the plan or the amount actually contributed to the plan |

Premiums higher for plans that provide larger benefits or greater contributions. |

Plans paying highest premiums will typically not have higher guarantees due to the small size of the maximum guarantee. Creates incentive to make lower contributions to avoid higher premiums. |

|

An amount that is assessed when a company withdraws from a plan |

Ties premium to events that often cause financial distress for plans. |

Fears over withdrawal liability are already a barrier to employer participation in the system. May not be able to collect the premium if the employer is bankrupt. |

|

A premium that represents a portion of the investment gains of plans |

Premiums are highest when plans are most able to afford them. |

Highly unpredictable revenue stream for PBGC and negatively correlated with risk of additional financial assistance. |

|

Premium withheld from participant benefit payments |

Premiums are effectively paid by individuals receiving PBGC guarantee protection. Due to a large potential revenue base, a small withholding percentage could generate significant premium revenue. |

Despite small size, it is equivalent to a benefit cut applied to all retirees. |

In addition to higher premiums and alternative premium structures, some have suggested legislative action could assist PBGC by allocating general tax revenue as a supplement to PBGC premiums or impose a tax dedicated to PBGC, perhaps targeting transactions in a specific industry or industries whose plans are expected to need substantial financial assistance even while much of the industry is healthy. For example, an interstate freight tax could be dedicated to transportation industry multiemployer pension plans. The Keep our Pension Promises Act (S. 1631 and H.R. 2844), introduced June 18, 2015, in the Senate, is an example of legislation that would generate additional funding for legacy pension benefits through the elimination of certain tax exemptions that do not apply to most taxpayers.

Another option is to authorize a transfer of assets or loan assets from the single-employer PBGC program or combine the two programs. A reduction of PBGC guaranteed benefit levels (from already low levels) or an increase in minimum required contributions could also be considered. All of these alternatives introduce a host of controversial issues that impact various stakeholders in different ways and have economic and fiscal impact that are beyond the scope of this issue brief.

Conclusion

PBGC, the guarantor behind the guarantee for struggling multiemployer pension plans, is facing significant challenges and risks caused by a confluence of economic, demographic, and industry-specific events.

Unfortunately, there is simply not enough money in the system currently to support existing multiemployer PBGC guarantees. This cost will ultimately be borne by some combination of plan participants, employers, or taxpayers.

While there are no easy solutions, it is imperative that all stakeholders work together to find a way forward to strengthen the multiemployer pension system. To do nothing leaves the system on a path toward an inevitable failure to pay benefits that were intended to be guaranteed, which would result in catastrophic benefit losses to hundreds of thousands of participants.

PBGC Multiemployer Program At-A-Glance

|

|

|

Year |

2025 |

2035 |

|

Probability of Insolvency |

50% |

98% |

|

Mean Projection |

|

Assets |

$ 0 |

$ 0 |

|

Premium Revenue |

$ 385 |

$ 566 |

|

Financial Assistance |

$ 2,254 |

$ 4,046 |

|

Percentage of Financial Assistance Payable |

17% |

14% |

Source: PBGC (Dollar amounts in millions)

|

|

-

PBGC insures about 1,400 multiemployer pension plans covering more than 10 million participants.

-

PBGC multiemployer plan premium levels and guaranteed benefit levels are significantly lower than those provided for single-employer plans.

|

-

At the current premium level, there is more than a 50 percent chance that PBGC’s multiemployer assets will be exhausted by 2025 and a 98 percent likelihood by 2035.

-

If PBGC’s multiemployer program exhausts its assets, participants receiving PBGC support could see their guaranteed benefits reduced by approximately 85 percent. When compared to the original benefit earned in the plan, the reduction is even greater. For example, a 30-year career participant entitled to a $26,000 annual benefit from their plan might first see a reduction to $12,870 (PBGC’s maximum for someone with 30 years of service) when the plan is first eligible for PBGC financial assistance, but then ultimately to about $2,000 per year upon the exhaustion of PBGC assets.*

-

Most of the growth in PBGC financial assistance claims is expected to occur between 2023 and 2029 when Central States and a number of other large plans are expected to become insolvent.

-

Based on PBGC’s 2016 MPRA report, premiums would need to increase approximately 6 times current levels to cover expected financial assistance payments through 2035, with even larger increases necessary to assure longer-term solvency.

* For additional details on the how the participants may be affected by PBGC guarantee levels see the March 2015, PBGC’s Multiemployer Guarantee Report.

Note: The statistics shown in this box as well as throughout this Issue Brief are based on PBGC’s 2016 MPRA Report and the FY 2015 PBGC Projections Report. |

|

1 PBGC also guarantees benefits for single-employer plans: a program with separate premiums, benefit guarantee levels, and financial/delivery structure. This program is not covered in this issue brief. “Insolvent” for purposes of this issue brief means a pension plan has insufficient assets to pay current benefits due under the plan.

2 The data in the chart is based on PBGC’s average (mean) projected financial assistance amounts. The average financial assistance is taken from PBGC’s ME-PIMS model results, which look at a variety of future economic paths. The ME-PIMS model simulates financial assistance payments from PBGC to insolvent multiemployer plans to pay retiree benefits and maintain the plans.